Deal Analysis · 8 min read · Updated June 2026

How to Analyze an Income-Producing Property Before Making an Offer

The offer is the moment the deal is won or lost. By the time you sign, you should already know what the property earns, what it costs to run, and how it performs under stress. This is the framework I use with investor buyers before recommending an offer price.

Step 1 — Validate the income

Pull the current rent roll, T-12, and lease copies. Compare contract rents to market rents using three live comparables, not Zillow estimates. Note any concessions, free months, or below-market leases.

If income data is missing or sloppy, treat that as diligence information. Sellers with clean books usually run cleaner properties.

Step 2 — Rebuild the expenses

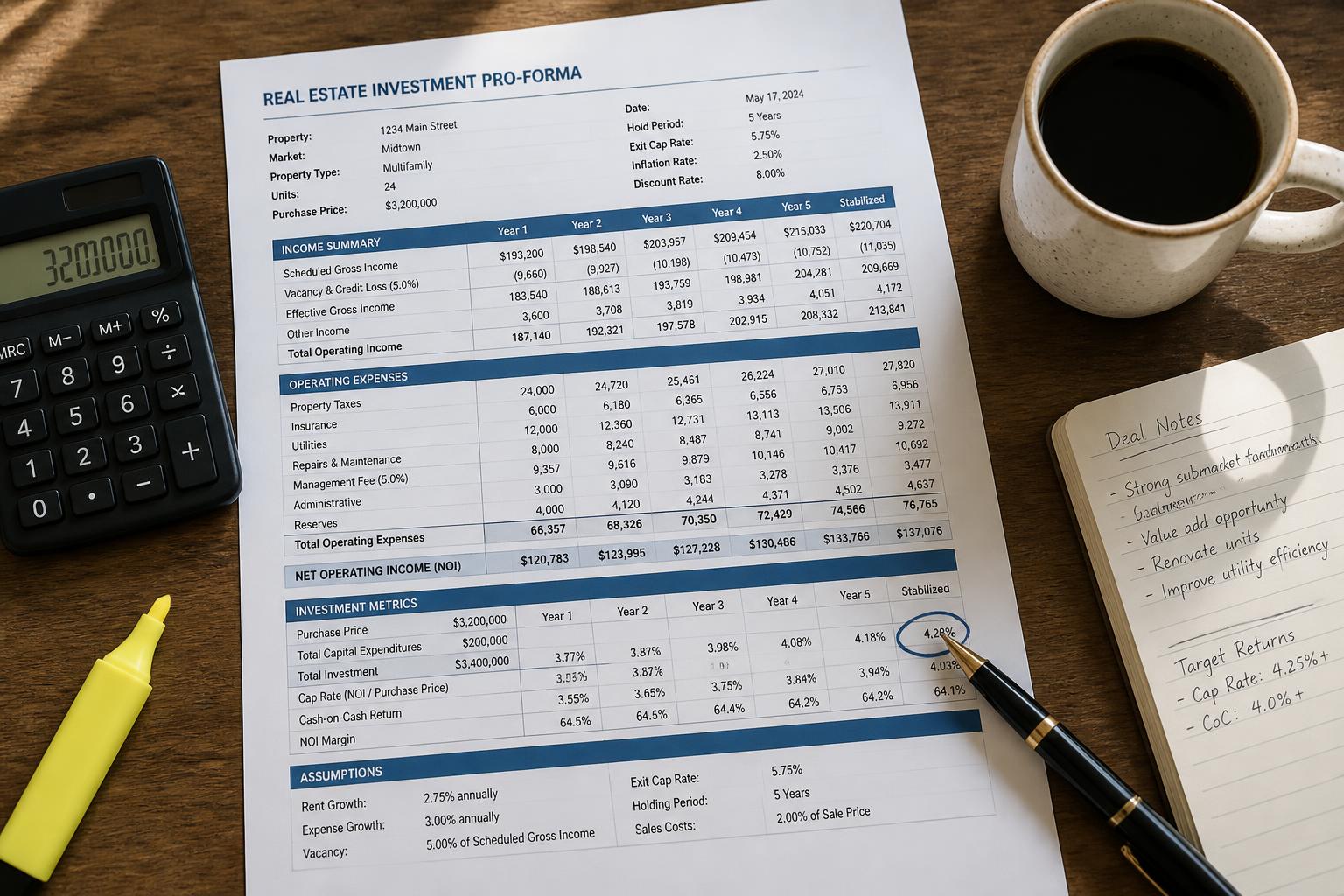

Don't trust the seller's expense ratio. Rebuild taxes (re-assessed), insurance (quote, don't assume), management, repairs/maintenance, CapEx reserve, utilities, and any payroll.

Most amateur pro formas underweight CapEx and management. Bake both in at realistic numbers even if you self-manage today.

Step 3 — Layer the debt

Use real lender quotes: rate, amortization, term, prepay. Model both your base case and a -10% rent / +15% expense stress case. A deal that breaks under stress is a deal that needs a better price.

Step 4 — Compute the returns that matter

NOI, cap rate, cash-on-cash, debt-service coverage, and a five-year IRR if you can. Compare to your alternative uses of capital — not to a generic market benchmark.

Step 5 — Walk the property and reconcile

The model lies; the walk-through tells the truth. Compare the building's condition to your CapEx reserve and the rent roll to what you see in the units. Adjust your offer, not your assumptions.

Key takeaways

What to remember.

- Validate income with live comps, not online estimates.

- Rebuild expenses from scratch every time.

- Stress-test debt and rent before you offer.

- Walk the property and reconcile to your model.

FAQs

Frequently asked questions.

How long should pre-offer analysis take?

For a stabilized small rental, 60–90 minutes once you have the data. Commercial, storage, and RV parks usually take 3–6 hours of focused work before a credible offer.

What's the most common mistake new investors make?

Trusting the seller's expense ratio and missing the re-assessed property tax line. Together those errors create the bulk of disappointed first-year cash flow.

Do I need a CPA or partner to analyze a deal?

Not for the operating model. For tax structuring and entity choice, yes — bring in a CPA before closing the first deal.